Everyone on the street was hoping that June would bring a reprieve to the selling pressure experienced in May but if the first day of the new month was any indication fasten your seat belts!

Market volatility has returned with a vengeance and I don't see anything coming up during the month that is going to change that. The Euro zone is approaching its moment of truth and unless Germany blinks to the pressure to change some of its policy paradigms the health of the global financial system is at risk. Will they blink?

We'll be looking at where the markets are after a bloody week and I'll be presenting a technical and fundamental thesis on why I believe we'll see a technical bounce in stocks next week. I'll also be addressing the other question mark, China, and examine the soft landing/hard landing theses . But let's look at some charts!

The Dow Industrials had its worst week of the year and wiped out all its gains for 2012. Almost the entire decline took place on Friday on the heels of a miserable monthly employment report. Here's a daily chart of the Dow:

(click on chart for larger image)

I know the chart is a bit busy but just take away that the Dow is now trading below its 200 day moving average and the 61.8% Fibonacci retracement level (purple arrow) is the "line in the sand". If we do not stabilize here we're looking at Dow 11,800, 11,500 or as low as 11,200 (these are rough projections based on multiple Fibonacci retracement levels). Will we hold the 61.8% Fibonacci retracement level? I won't stick my neck out on this one as the market is being held captive to headline risk. I do feel reasonably comfortable for reasons I'll state later that we will not penetrate this level in the coming week.Here's the Wilshire 5000 Index which reflects all stocks actively traded in the US:

It too has penetrated its 200 day moving average and also pierced a Fibonacci cluster (brown arrow). I want to call your attention to the slight divergence in the RSI momentum indicator in the top panel. This is incidental evidence that downside momentum is waning. I'll have more on this below.

All in all, stocks had a brutal week! But here's why I believe we will see a short term bounce this coming week:

This is a daily chart of the Euro and you can clearly see it's steep decline in May. Again, sorry for all the Fibonacci levels but I circled the most important item on the chart which was Friday's key reversal where the Euro opened below Thursday's close but closed above Thursday's open. This is known as a "bullish engulfing pattern" in candlestick charting. It usually signifies a change in investor sentiment. Now, no signal is guaranteed in the market but these patterns, like the Fibonacci retracement levels, are uncanny in their prophecy of future market movements. I'm looking for a pop in the Euro to the short term Fibonacci resistance at around the 126.60 level.

Fundamentally, the terrible monthly employment report negatively impacted the Dollar and a short covering rally ensued. I'm expecting more follow thru this week as the Euro is severely oversold and the Dollar is extremely overbought.

Another factor that will drive this short term rally is that the net speculative short position reflected on the CFTC (Commodity Futures Trading Commission) Commitment of Traders report of 5/29 was a record 203.4k. When we have this kind of imbalance in the Futures market any move up in the Euro will spark a wave of short covering that feeds the ongoing rally until the "weak hands" are squeezed out of their positions.

The London FOREX (Foreign Exchange) market is closed on Monday and Tuesday and it will be interesting to see how the lack of liquidity will effect currency trading.

What does all this have to do with stocks? Remember our correlations. The US Dollar moves inversely to stocks. As the Dollar Index rallies, stocks and commodities weaken. But the Euro comprises 57% of the Dollar Index and so has the most influence on Dollar pricing. In the overwhelming majority of cases, a strong Euro means a weaker Dollar and therefore, a higher stock market.

And here's a daily chart of the US Dollar that clearly reflects the rush into the safe haven trade:

There's no real sign of weakness here but the top panel is signalling a severely overbought condition and the MACD in the bottom panel is giving the very slightest hint of weakening.

Please understand, I'm talking about a short term bounce in stocks next week. I'm bearish on the market going into the summer unless Europe gets its act together. More on that subject below.

Treasuries had another historical week finishing at all time highs. And the safe haven flows even impacted other debt markets that are seen as "safe". Even British Gilts recorded the lowest yields since the Bank of England was founded in 1703! Yields on German Bunds, Europe's safe haven trade, recorded record lows as well.

Here are two long term charts to give my readers some perspective of the great bull market in bonds going back to 1981. The first is a monthly chart of the yield on the 10 Year Treasury Note:

I'll say three things here about Treasuries:

1. Depending on how events unfold in Europe we could actually see lower yields! One percent on the Ten Year anyone? (I'm not kidding)

2. Both charts speak to massive deflationary forces gathering steam in the global economy

3. This will be the next great bubble to burst. I can't see anyway to unwind this market in a benign fashion. But that's a subject for a commentary on its own. :-)

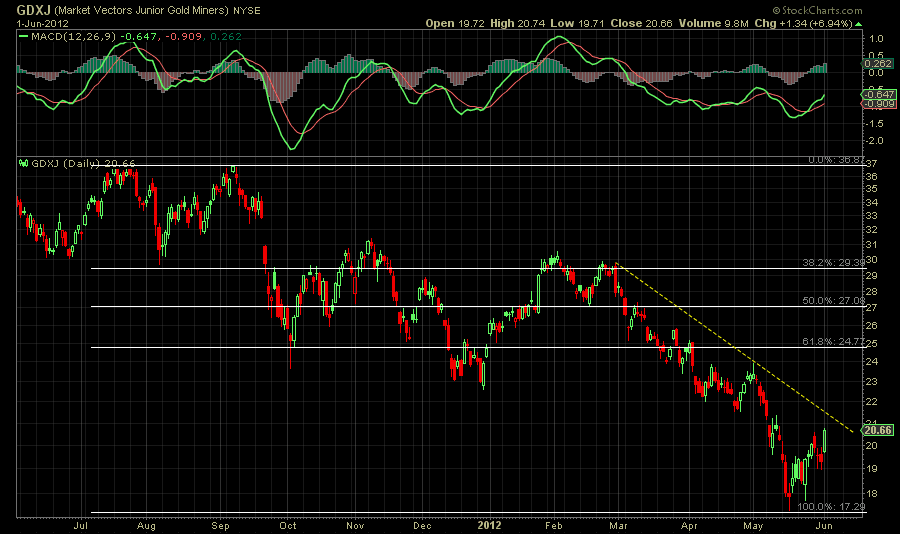

Let's look at Gold. It sprung to life on Friday as global fear gripped risk assets:

Gold's price action has been confounding many on the street (including me) and Friday's price action was no different. Many are now saying that the Gold market is anticipating central bank liquidity injections (aka QE or money printing) but I'm ambivalent on that reason. But what is different about this move is that the Gold mining stocks have been forecasting this move in the "yellow metal" for some weeks now:

GDXJ has yet to penetrate it's multi month downtrend line but is clearly following its big brother.

We should find out soon if this gold rally is real. If the popular thesis that gold is rallying on perceived central bank monetary easing then precious metals should continue to rally if we get any news from central banks alluding to more QE. If they resume their slide on such news then this was nothing more than a quirky bounce by confused investors who can't get a handle on whether Gold is an inflation hedge, a safe haven or neither!

Commodities, which was the first asset class to give us the forewarning of market weakness back in February, are in free fall. Two charts tell it all. Here's a daily chart of Brent North Sea Crude Oil:

As you can see oil clearly fell out of bed this week but I also want you to notice that it is the first time since last October (yellow arrow) it has closed under $100.00/barrel. Friday's price action (pink arrow) is the lowest price since February 2011.

And here's the Commodity Research Bureau Index (CRB) which is comprised of 19 different agricultural, livestock and industrial metal commodities:

Euro zone

It's truly a challenge trying to understand possible scenarios that could develop out of the Euro zone. There is a tangled web of political and financial entities that have a say on the daily news events that are moving these markets. I'm going to attempt to make this as simple as possible for my readers. If you've been following the events or reading my commentaries then you have a pretty good background on the issues.

We have bank runs in Spain, Greece, and now Portugal? Spain was rebuffed this week by the ECB after requesting funding to bail out Spanish banks that desperately need recapitalizing for ongoing real estate bad loans. This means Spain has to recapitalize their banks themselves. But they don't have the money. So they have to sell debt in the bond market to finance the recapitalization. But everyone knows their banks are in trouble so they will demand higher interest rates to buy the debt. But Spain's financing rates are already unsustainable which only makes creditors want higher rates. What a negative feedback loop! The same situation in Ireland and Portugal in the past few years forced them to turn to the EU for a bailout. But the EU does not have the funds to bailout Spain.

Greece now has a ban on any more opinion polls regarding the election on June 17th so the market will be in the dark on any understanding of who will come out on top in that election. An immediate Greek exit from the Union is not a done deal if the anti austerity SYRIZA party wins but I suspect that an eventual exit is inevitable. SYRIZA leader Alexis Tsipras, if he is elected, wants to gamble that the EU will back down from its threats to cut Greece off of any funding if they break their agreement with the EU made earlier in the year. I won't go into the reasons why the EU's hands are almost tied in this matter but I'll end this by saying: don't dare the Germans! More importantly, even if the pro austerity faction wins the election, the Greek situation is utterly unsustainable. The country, financially and economically, can be likened to a dead person who's heart is kept beating via life support.

More and more European leaders are attempting to put pressure on Germany to ease up on austerity and promote growth. The problem with their formulation is that their idea of growth is a money printing bail out. And Germany, who is the EU creditor, knows it will be on the hook for the debt when it's all over. So Germany will not acquiesce to the pressure and wants substantial fiscal concessions before going along with the money printing. And even then they are uncomfortable with the idea of inflating the European monetary base to accomplish "growth". But I do believe that the Germans would go along with France's Hollande's idea of growth if they did get those concessions.

In last weeks commentary I gave the formula for German agreement on all the "ideas" coming out of other member states to solve the problem:

Relaxation of austerity must equal relinquishing national fiscal sovereignty.

This is the European quandary. Will individual countries agree to, in essence, give up their sovereignty in order to benefit from being in a wider union? Or will Germany give in and write a blank check in order to save the union? I can tell you now that Germany will not write a blank check. So, will individual member states surrender their sovereignty?

I've addressed this fundamental issue many times since I started composing these commentaries two plus years ago. While I don't see the the German requirement being agreed to by other member states at this time, the chances are better that member states cave in to Berlin. Interestingly, Spain's Rajoy was on the airwaves yesterday (Saturday) calling for a new fiscal authority in the euro zone which would "control and harmonize national budgets and manage European debts".

So we have the member nations of the EU at loggerheads with each other. How does the dilemma resolve itself? It's impossible to know how this crisis will end. We just need to protect ourselves and understand how various possible scenarios may play out and how we position ourselves for them. However, due to the fluid nature of the crisis it's impossible to make detailed predictions regarding market movements more than one week into the future.

In the short term, look for a probable interest rate cut from the ECB this week. Initially, this will support the Euro and provide the bounce up to the 126.60 level I alluded to above. However, any indication from ECB President Mario Draghi that the ECB will resume purchases of periphery debt in the open market will ignite a short term risk rally. Otherwise, continued wrangling between the "pro austerity" and "pro growth" factions in the EU will continue and because of that market volatility will continue.

China

China is clearly the next big worry that's bearing down on our markets. But it is more than just China; it the entire global economy that is slowing. Here's the MSCI Emerging Markets Index Fund which tracks the performance of publicly traded securities in emerging markets. It includes the BRICS (Brazil, Russia, India, China, South Africa):

There's a multi year head and shoulders formation developing on the chart but I haven't outlined it. I'll let my readers study the chart to determine whether they can see it. The important point of the chart is the black dashed line. We are nowhere near the lows formed last October and we have a ways to go before we penetrate that neckline on the chart. So while we are slowing down globally it's not time to panic (yet). Also notice the MACD indicator in the top panel has turned up.

Here's where it gets interesting. This is a daily chart of the Dow Jones China Index:

We have an inverse head and shoulders formation developing and it is on the cusp of fruition. It already made one failed attempt to break out in the first week of May but the formation is still valid until we see a significant deterioration in the price action.

On a fundamental level, the street is hoping for a significant stimulus package out of the Chinese government any day now. I read an article in Barron's this weekend and they interviewed Dong Tao, an economist at Credit Suisse who is on the ground in China (Hong Kong specifically). He's of the opinion that the Chinese will not react to the present slowdown the way they did in the midst of the GFC (Great Financial Crisis). Back then they pumped 635 Billion to jump start the Chinese economy. This time, they are simply bringing forward pending infrastructure and industrial projects originally slated for 2013 and 2014 and funding them this year. This funding is pumping 157 Billion into the Chinese economy.

The Chinese are wise to stimulate in this way. They realize that they are the tail the dog is wagging. They are primarily an exporting economy, not a consumer based economy. And they are suffering from reduced exports due to slowing demand around the globe, especially with their biggest trading partner, Europe. And so their economy is captive to the economic condition of their trading partners. So, it's not so much that as China goes so goes the global economy but rather as the global economy goes so goes China.

In any event, I still see a soft landing for the Chinese economy and have been heartened lately by the relative stabilization in price action in their major indexes.

The economic reports coming out this week in the US will move these markets but we also have a host of FED Governors scheduled to speak this week starting on Tuesday and the markets will be dissecting every word that is said. The culmination of all these talks will be Ben Bernanke on Thursday morning when he testifies before the Joint Economic Committee on the economic outlook in Washington.

Other noteworthy reports that could move markets:

Monday - Factory orders - in the absence of any significant news event, any significant weakness will fuel further downside in the market. A neutral or better than expected report will be ignored.

Tuesday - ISM Non Manufacturing Index - could be a market mover. But again, it will only be if there is no other significant news out there.

Thursday - Jobless claims - will be closely watched for confirmation of this past week's dismal employment report that ignited the sell off on Friday. Any significantly better than consensus reading will spark a rally.

And Ben Bernanke speaks at 10AM.

Friday - International Trade - could move markets depending on the emotional tenor of the market after Bernanke speaks.

In Europe:

Wednesday - EMU Economic Sentiment

Thursday - Italian Consumer Price Index - will be closely watched to determine the depth of the economic contraction going on in that country.

- EMU HICP Flash Index ( harmonized index of consumer prices) - the ECB uses this as its measure of inflation in the Euro zone.

Friday - German PMI (Purchasing Managers Index) - will be watched closely to determine how quickly and to what extent the German economy is slowing.

All these reports/events I've cited above will be ignored depending on news flashes emanating from Europe, central banks or both. Any inkling that EU member states are willing to sit down and broach the matter of fiscal union will be embraced by risk assets. Any substantive pronouncements regarding the same will ignite a world wide rally in stocks. At the same time, any statements smacking of intransigence in negotiating any matters relating to any of the above will promote further selling pressure in global risk assets.

I started the commentary by stating that we are living in historic times but we're also living in dangerous times. The world is being held captive to a few European politicians. And based on history, we cannot be assured of a positive outcome. Let us hope that sanity will prevail.

Have a great week!

NOTHING IN THIS COMMENTARY SHOULD BE CONSTRUED AS AN OFFER OR ADVICE TO BUY OR SELL ANY SECURITIES, OPTIONS, FUTURES OR COMMODITIES. THE OPINIONS ARTICULATED ARE ONLY THIS AUTHOR'S WHO IS NOT A LICENSED INVESTMENT COUNSELOR OR BROKER

No comments:

Post a Comment