Mario Draghi became a close friend to the financial markets this week when he announced early on Thursday morning "unlimited bond buying" or in the new vernacular of the Euro zone crisis "outright monetary transactions" in order to shore up southern periphery debt woes. For the most part, his announcement lifted global equity markets that had been weighed down by fears that a politically and financially frayed European Union was on the cusp of imploding.

China also had a small part in allaying investor concerns this week by announcing early on Friday a 175 billion infrastructure spending package to stimulate their moribund economy.

I'll be addressing some of the challenges Mr. Draghi will have in implementing his bond buying program along with the most probable outcome to the FOMC meeting that's taking place this week.

Stocks had a banner week with most of the indexes up north of 2% while mid caps and small caps closed in on the 4% range.

Here's the Dow Jones industrial Index and it finished the week exceeding its previous post crash high set on May 1st of 13,279.32. The Draghi "put" turned this market around on a dime. Risk is on!

(click on charts for larger image)

Below is a weekly chart of the Russell 2000 small cap index. Small and mid cap stocks are leading this market higher in the short term (see bottom panel) and this is just the leadership we want to see for a healthy stock market. We'll want to see this trend continue to confirm the health of this "bull".

Lastly, here's a weekly chart of the S&P 500 which also recorded new post crash all time highs on Friday:

In order to determine where resistance may lie on the S&P we have to go all the way back to March 2008 at around the time of the Bear Stearns collapse when the S&P was trading at the 1445-1450 level. There appears to be some pretty thick resistance at the 1445 - 1465 level but with the assurance of central bank liquidity in Europe and probably here in the US after this week's FOMC meeting we're liable to cut thru this resistance like a hot knife thru butter!

To give my readers a perspective on where we are in relation to pre Lehman days below is a chart of the S&P going back to the all time highs made back in 2007:

The blue arrow is Friday's close. The pink arrow was the all time intra day high of 1,576.09 made in October 2007.

True to our inverse correlations, Treasuries corrected but the price action on Friday was pronounced to the downside. Here's the iShares Barclays 20+ Year Treasury Bond Fund (TLT):

There are a few points I want my readers to notice. The stubby red arrow points to Friday's close where it looks like TLT literally dropped thru a trap door. But when I put some Fibonacci lines on the chart I noticed that the rally treasuries had been experiencing off of the lows set in mid August did an about face at the 61.8% retracement level. This is a classic technical stopping point when there's a short term rally in an ongoing down trend.

More and more prognosticators are calling for an end to the historic bull market in bonds we have been living with for the last 30 years. And while I agree it has to end soon and that we are obviously closing in on that end, I'm not willing to say we've seen a top in this market. Here's a weekly chart of TLT to give my readers a greater perspective.

I've highlighted the post Lehman high in early December 2008 and circled where we are in the past month. We clearly have a long way to go before we declare the bond bull market dead. I'd be looking for a break under 110 to start taking the death knell of the bond market seriously.

Still, we need to understand that fundamentally what occurred this week in Europe was a true game changer which could provide the catalyst for a bear market in bonds.

Gold was the major beneficiary of Draghi's announcement this week:

Gold is obviously reacting to the prospect of central bank money printing and I have no good reason to tell my readers that they should not be investing in the yellow metal. Certainly, I will probably take a short term bullish position before the FOMC's announcement on Thursday but I'm not comfortable in saying Gold is a buy and hold investment into 2013. I'll need to see more definitive policy pronouncements out of the FED and the ECB before I commit myself to trading this uptrend. I'll have more on Gold and the ECB below in my analysis.

Commodities did not immediately react to the ECB announcement on Thursday like I thought they would but took off on Friday based on the news out of China that the government was going to pour the better part of 200 billion dollars into infrastructure projects.

Here's is an update of the same weekly chart I posted in last week's commentary. It is the Dow Jones UBS Industrial Metals index which is composed of four futures contracts on industrial metals, three of which (aluminum, nickel and zinc) are traded on the London Metal Exchange and the other of which (copper) is traded on the COMEX division of the New York Mercantile Exchange:

I had made the point last week that support had been holding at the 140 level for 11 weeks and thus was a potentially bullish signal as the longer support held the more likely the index would turn higher. Well, we had a break out this week due to Friday's move and any follow thru next week will confirm this bullish indication.

Finally, the currency market has confirmed the "risk on" bias in global markets:

Here's a daily chart of the Dollar and we broke thru some significant short term support (yellow line) this week and like Treasuries, the Dollar fell out of bed on Friday.

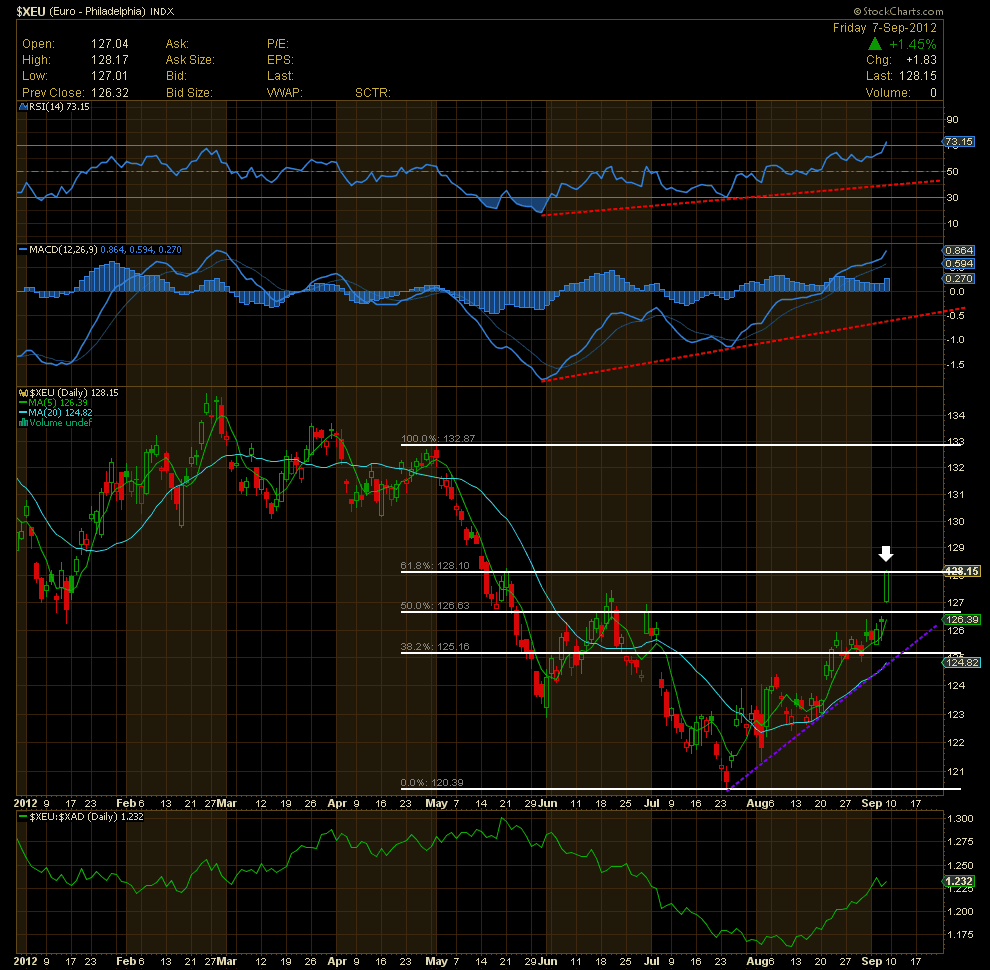

The Euro, of course, being roughly 57% of the Dollar index, has rallied to 128.15 and is presently sitting on Fibonacci resistance:

As I pointed out above with Treasuries, the 61.8% retracement area is a classic turn around area where if this is just a short term rally in a longer term downtrend the Euro should back off at these levels. Will it?

The answer to my question is more complicated than just appealing to technicals or the classic inter market relationships which have guided our understanding of where these markets are heading. Let me just say that fundamentally the Euro should start to weaken here but the price action in the short term will be skewed if/when Bernanke and Company announce another round of QE. Also, there is a distinct possibility that the Euro may be ending it's leading role as a "risk on" currency and it's position may be usurped by the Aussie Dollar:

I'll end this segment of the commentary with this. I have not yet worked thru all the issues related to the thesis I've posited in this section of the commentary. There are many crosscurrents in the Foreign Exchange (FOREX) Market and I always laugh when I see advertisements on CNBC attempting to entice investors by stating that trading currencies is relatively easy because there's only a handful of currency pairs. Currency markets are the most challenging and treacherous markets in the world to understand and statistics point out that 80% of investors who get involved trading currencies blow up their accounts. I very rarely trade currencies but they are extremely helpful in assisting me on the direction of other risk assets.

Analysis

It's pretty clear that we have experienced a significant short term turn in equities as a result of Mario Draghi's plan to bolster southern periphery debt. But is the turn something more than just short term?

If you asked that question last week when details of the plan were being leaked to the international press the overwhelming response from the Wall Street intelligentsia would have been no. But post news it seems opinions are evenly split.

Let's understand what Draghi's plan does. It buys time! It cannot solve the insolvency issues that these countries are burdened with. Given the strictures and the almost overwhelming political/cultural hurdles that the European Union has to overcome with no kind of federal system as we have here in this country, Draghi's proposal goes as far as it can to put the biggest band aid on the problem we

have seen to date as well as placate any dissenting factions in the union (specifically, Germany).

What is he offering?

1. Potentially unlimited bond buying of debt in the secondary market. The ESM would buy any primary debt as necessary.

2. Sterilized purchases (meaning as he prints money to buy say, Spanish debt, he takes that same amount of money out of the system somewhere else). This was probably the point that the northern periphery, particularly Germany, needed in order to grudgingly accept the plan.

3. The ECB will not demand senior status for the bonds it buys; meaning if Spain were to theoretically default the ECB would be treated equally with other investors in the apportioning of any remaining assets remaining after the default.

What does the plan want in return?

1. Any country seeking ECB assistance must formally request aid to the ESM (European Stability Mechanism) and as a result, assuming the ECB believed they were qualified for the bailout, would be subject to additional requirements to clean up their deficits (aka more austerity). If any country agreed to the conditions and then reneged on the agreement the ESM & ECB would stop supporting their debt in the market.

Are there any holes in the plan?

1. The ESM has not been ratified by the German Supreme Court. That decisions comes this week (9/12). Most experts believe the odds favor a positive verdict but the court may decide to place impediments on a positive verdict like requiring the German lower house to approve any amounts Germany would be required to deposit into the fund or even imposing a required limit of money the Germans may be responsible for. Any impediments that smack of limiting German support to the fund will not sit well with risk assets.

2. It's almost impossible to offer potentially unlimited bond buying but then say you're going to sterilize the purchases. At some point the ECB can only manipulate the monetary system so much before they can no longer take out of other areas what they're putting in to an Italian or Spanish debt market. And this is why Gold is sensing inflation. If the ECB were forced to buy say, 300 billion Euros in Spanish debt, there is no way they could effectively sterilize that amount of money.

3. Spain, the country which has been the major impetus behind formulating the plan, has so far not asked for assistance. Rajoy wants to know what the conditions are first. So, Draghi has formulated a plan that is as good as it gets considering the financial/political framework he has to work with but until someone asks for help the plan sits on a shelf gathering dust!

Now, Spain will eventually be forced to ask for the help because they have 30 billion in bond redemptions coming due at the end of October and they don't have the money to honor their commitments. But there will be some wrangling and back room deals because Rajoy will not accept any conditions that would include cutting pensions for retired and present government workers.

So why do I think the plan is such a game changer? Look at Spanish and Italian bond yields. Just the announcement caused yields across the yield curve of both countries to drop and by almost 1% on the long end of the curve alone! In essence, Draghi and the ECB have gotten what they wanted without printing a Euro. The gargantuan bond market believes in the plan and in Mr. Draghi's resolve to implement it!

Secondly, this week's outcome shows that Germany's position has softened. I stated last week that Merkel's endorsement of the ECB plan essentially hung Bundesbank President Jens Weidemann, the only dissenter on the ECB policymaking committee, out to dry. As I said last week Merkel knows the can can't be kicked down the street any longer. She could stall with Greece, Portugal and Ireland. Spain and Greece are to big to play political Russian roullete with the market.

Third, the issue of sterilization mentioned above will eventually become untenable for the reasons I stated. If there's a huge demand to support either Italian and Spanish debt everyone knows, even the Germans, that there will have to be unsterilized purchases. This supports my thesis that the Germans, outside of Weidemann, have capitulated on their hard anti inflationary stance.

Fourth, what if Spain or Italy (more likely) agrees to the conditions that are set by the ESF and the ECB and then renege on the agreement? Will the ECB really stop supporting them? In such a scenario, if ECB support were to cease, a chain of events would commence that would end with the disintergration of the Euro zone as we know it.

Euro zone debt problems will be with us for years but this week's event finally effectively eliminated the probability of a global financial meltdown. Don't misunderstand. We'll still get some spooky headlines and scary days because of unresolved issues in Europe (Greece, etc.) but Mr. Draghi can be credited with putting the finishing touches on global financial stability in the wake of the greatest financial crisis since the Great Depression.

As far as Greece goes, expect some wrangling around their request for an extension to meet austerity targets but expect that inevitably they will be granted an extension. Already we're getting positive reports out of the "Troika" that have been in the country on a fact finding mission to determine whether the Greeks are meeting their austerity targets. Already, the tenor of the reports are changing, indicating a softening stance toward Samaris's efforts to reign in the country's deficit even if the country is not meeting its targets.

And one more thing, I incorrectly stated last week's commentary that the Dutch election would be on 9/6. In fact it's on 9/12 but it now appears to be a non event. The Socialists, who are anti EU and anti bailout, were leading in the polls but after the socialist candidate either debated or had a few appearances on Dutch media, it appears he put his foot in his mouth. Expect the present party in power to remain there.

So it's OK to pour our money into the stock market again? Not so fast! Europe is still contracting and as long as that persists it will continue to hamper any growth in emerging markets and as an extension, global growth. I've stated before that unless you're investing time frame is over eight to ten years then this is not a buy and hold market. But if the Europeans can continue to successfully buy time in order for periphery countries to unwind their onerous debt and if we, in this country, can get back to a more capitalistically oriented economic policy, I'm willing to say the investing time frame alluded to above can be shortened to three to five years.

Here in this country the big event this week is the FOMC meeting on Wednesday and Thursday. Most are now anticipating QE3 and the rumor is that the FED will announce open ended bond purchases (mostly mortgage backed securities). Some felt that if Friday's employment report were better than expected the FED might not act. My opinion was that the FED's mind was made up in mid August and even a good employment report wouldn't have changed the path they were following. But Friday's report was absolutely horrid! There was virtually nothing positive to draw from the report. So look for another liquidity induced rally on Thursday as the FED pours more unsterilized money in our system.

All these factors are now suggesting we are going to see a significant rally in stocks going into the election. There will always be some lingering problems out of the Euro zone and exogenous events that will roil our markets. One of those exogenous events might be that the Israelis are still threatening that an attack against Iran is imminent. I've already stated in my commentary of 8/24 that recent research out of Stratfor in Austin, Texas documents that the Israelis do not have the capability to successfully strike these facilities, let alone knock them out for these reasons:

1. The Israelis only have a limited number of aircraft that have the range and can carry the necessary payload to do the job (if indeed the payload can do the job, see point 3).

2. Everyone remembers when the Israelis knocked out Saddam Hussein's nuclear facilities in1981 but this threatened attack is a different ballgame altogether. The distance to the target and issues surrounding air space violations make a successful attack against the Iranian facilities a formidable challenge.

3. Even if the Israeli Air Force can reach the target the facility in question is so deep inside a mountain that even a tactical nuclear devise detonated over the target would probably not knock out the facility.

If the Israelis want to take out the facility they've got to take it out from the inside. I won't deny that they have the ingenuity to do this but an airstrike will not work.

All this doesn't mean they won't try but I'm still betting against an attack. In any case, this will be a one day event and won't derail what I see as a significant intermediate term rally.

The only issue on the horizon that remains unresolved is the fiscal cliff in this country. First of all, look for some truce between the parties extending the cuts into early 2013 so we can get the elections and a lame duck Congress out of the way. But I'm not saying an extension is a done deal. If we learned anything from events in Washington in 2011, grid lock is becoming a way of life inside the Beltway and we're likely to see intense fighting between the election and the New Year.

I'm not as confident as some are that we can avoid falling over the cliff. This is the way I see it:

1. If Obama wins the election but the Republicans win a majority in the Senate the Bush tax cuts will continue in 2013 and beyond regardless of Obama's power of veto. Indications are that the Republicans will take the House.

2. If Romney wins the election and Democrats retain the Senate we will have grid lock and we will fall off of the fiscal cliff.

3. The best outcome for the markets: either an Obama or Romney victory and the Republican take a majority in both houses.

*** As to point #3 above, I'm speaking strictly of market perceptions and reactions and am in no way implying it does not matter to me who is elected President. I don't want any hate mail from my audience :-)

If we cannot extend the Bush tax cuts into 2013 and beyond the impact on our economy will be great. We're running right around 2% GDP growth for 2012. The drag on the economy from higher taxes will push us to near or even recessionary levels. Couple that with weakening global growth and recessionary pressures will be firing on all cylinders. Look for 4th quarter earnings to give us our signals on the 2013 global economy.

That's it for this week.

NOTHING IN THIS COMMENTARY SHOULD BE CONSTRUED AS AN OFFER OR ADVICE TO BUY OR SELL ANY SECURITIES, OPTIONS, FUTURES OR COMMODITIES. THE OPINIONS ARTICULATED ARE ONLY THIS AUTHOR'S WHO IS NOT A REGISTERED INVESTMENT ADVISOR OR BROKER.

What they are doing is absolutely disgusting.

ReplyDeletehttp://stock-market-quantitative-easing.blogspot.com