I addressed the big event for the week in this blogpost (http://equitymaven.blogspot.com/2013/06/bernanke-pops-bubble.html ) and I'll be addressing it more in this commentary.

However, another potential crisis is also impacting global markets and it's emanating from China. Recent economic data out of that country has been lousy:

(click on chart for larger image)

Chart courtesy of Soberlook.com

The manufacturing PMI is in contraction territory and consumer confidence is dropping precipitously.

However, a more serious situation has developed. Along with a decline of capital inflows into China due to declining exports, the People's Bank of China (PBoC) is attempting to make local banks scale back on frothy credit expansion plans and efficiently manage their own liquidity. In the process the central bank has driven the seven day repo rate to as high as 28% earlier in the past week. The result has been an inverted yield curve where short term rates are higher than long term rates.

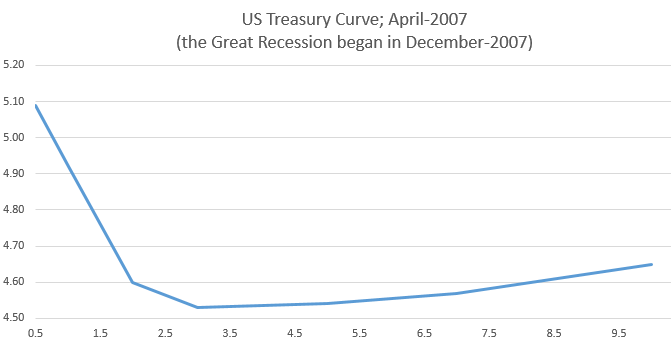

The two charts below are an historical comparison of the present Shanghai Inter Bank Offering Rate (SHIBOR) and the US Treasury curve in April 2007:

(click on chart for larger image)

Chart courtesy of Soberlook.com via Bloomberg and Markit

The PBOC did inject about 50 billion Yuan into the system on Thursday but it remains to be seen whether it is enough to loosen up the liquidity squeeze that has taken hold of the Chinese economy.

This is no small matter. The Chinese economy is in the same predicament we found ourselves during the fall of 2008 after Lehman imploded. The prospect that the world's largest exporting economy could slip into recession with the European continent still in the throes of recession will not bode well for the US economy or global financial markets.

All these problems are reflected on the daily chart of the Shanghai Composite Index:

(click on chart for larger image)

Next, the prospect that the Fed may be ready to take away the punch bowl along with a weak global economy helped take the struggling commodity complex to the mat once more. This was nowhere better manifested than in the precious metals. Here's a daily chart of spot gold:

(click on chart for larger image)

But industrial commodities which were already grievously wounded were battered again. Here's a daily chart of the Goldman Sachs GSCI Industrial Metals Index:

(click on chart for larger image)

Commodities are screaming deflation!

Technically, it looks like selling in our stock market may continue into next week as equities are being held captive to the Treasury market where yields had been moving higher but spiked after the Bernanke press conference on Wednesday. Here's a two year daily chart of the Ten Year Treasury bond yield:

(click on chart for larger image)

The street was watching the 2.5% psychological level. The concern was that if that level was broached it would be a possible signal that the Fed is losing control over interest rates. But technically, the 2.4% level was more important. We finished the seek at 2.514%, well above the technical and psychological level.

Analysis

Clearly, commodities were speaking to a deflationary threat for months but had been attempting an anemic comeback. However, now that the Fed has hinted that they may cut back asset purchases that trend is reasserting itself.

But the Fed only hinted at a tapering of asset purchases and with long term rates racing to the upside, the tepid recovery we are experiencing may be in danger. As stated on Wednesday's blogpost, I believe Bernanke deliberately used aggressive language in highlighting the Fed's possible plans in order to let some air out of the asset bubbles the Fed and other central banks have created. But I do not think that the Fed's is ready to imminently act to curtail MBS and Treasury purchases . Now Bernanke and company do believe, based on ongoing and possible future positive data streams, that the economy is strong enough to weather a cutback in their asset purchases. But what if it's not? And more importantly, with a cut back on asset purchases, does the Fed run the risk of losing control of the long end of the yield curve?

The fact of the matter is that the Fed only controlled "duration" in the Treasury market not by it's asset purchases which were formidable, but by "jawboning". And this highlights the psychological nature of financial markets.

With continued recession in other parts of the world and now with recent events in China, a serious deflationary environment threatens and may inevitably have to be met with more QE!

The situation in China is indicative of an extremely weak economy. In previous commentaries I have stated that China is the "tail the dog wags", meaning, as a leading exporter, it's economic health is dependent on the countries it exports to. And China's largest customer is not the US; it's Europe.

At the same time, I have stated in past commentaries that US equities are heading higher and have also proclaimed boldly that we are beginning a secular bull market that can be likened to the 1982 - 2000 bull market. And I still believe this is essentially true.

However, if our equity market is going to continue higher the other parts of the global economy are going to have to cooperate. China's issues are a warning for global financial markets. And the key to solving China's problems is Europe.

As of now, European economic prospects, while dim, have recently signaled that it maybe bottoming out. The key word here is "maybe". Until we see a trending improvement in economic data coming out of the Euro zone, the risk that the deflationary strangle hold that has been manifesting itself in commodities could put a lid on all equities, the US included. Next week there's a spate of Euro zone economic data being reported that will assist us in our determination of their economic prospects.

For now, all eyes in this country are on the Ten Year Treasury Note yield. On May 1st, the yield was as low as 1.613% intraday. On Friday (6/21) it closed at the highs of the day, 2.514%. Stocks normally like gradually rising interest rates in an economic recovery because it speaks to resilient business conditions. Increasing credit demand allows banks to raise rates to meet the demand. But the present situation is unlike a normal credit expansion cycle for two reasons:

1. The historical backdrop of the past four years and the central bank intervention needed to save the planet from financial Armageddon has distorted the relationship of yields to credit demand. Rates are artificially rising not necessarily because the economy is getting better (though it indeed might be) but because of the prospect that monetary stimulus is being taken away in anticipation of a credit expansion. It's like getting "the cart before the horse".

2. The precipitous rise in rates from May 1st suggests the rise is not due to improving economic conditions but because of distortions created by the Fed's QE. The incredible rise in rates in such a short time is more indicative of a move due to a crisis.

To sum up:

In the short term, until the rate of change in US interest rates stabilize (stop rising), we will continue to experience volatility in the stock market. The market at this time obviously does not believe that our economy can support these higher rates. But can our economy support these rising rates? My answer is that much will depend on events elsewhere in the world.

In the longer term, watch Europe and it's "tail", China. The deflationary nemesis that central banks have attempted to bury with reams of fiat money continues to rear it's ugly head in global markets. Whether we could slip into global deflation will have much to do with the timing surrounding these two questions: Will Europe's recession bottom out and improve in the second half of the year? And can PBoC to normalize their yield curve quickly?

Have a great week!

Nice analysis

ReplyDeleteThanks Vincent!

ReplyDelete