We're fast approaching the moment of truth in the market and I'm decidedly bearish on the outcome in the next few months. I'll be expanding on my rationale later in this commentary. For now, let's look at the charts:

(click on chart for larger view)

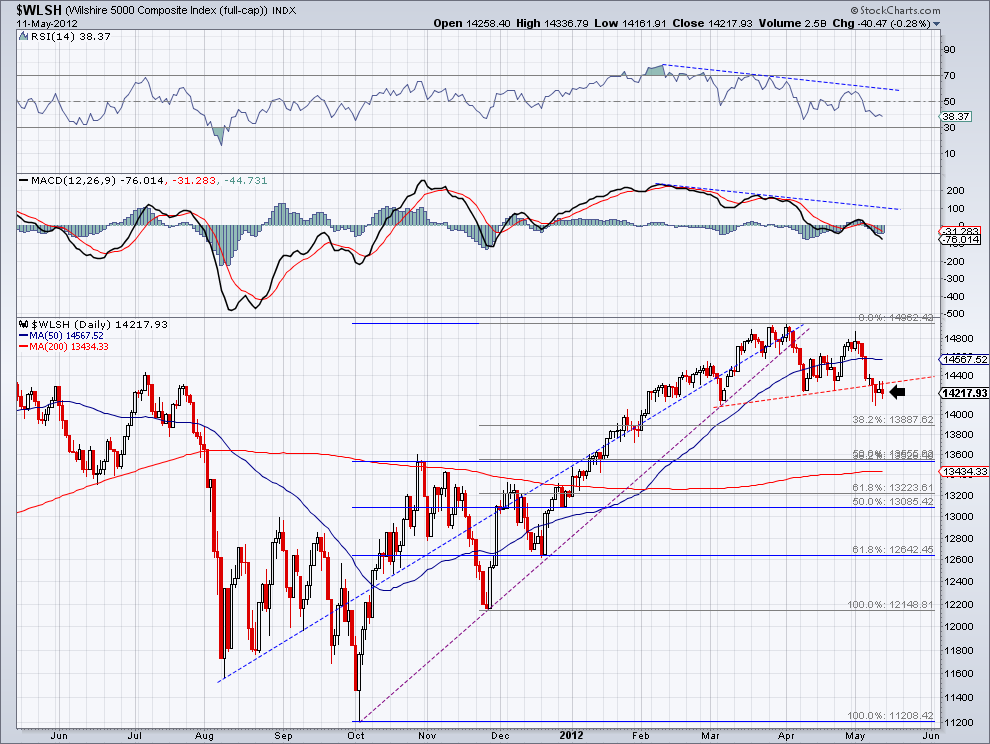

Normally, I would agree that the bounce off of the 783.60 support line is a positive technical development but the negative momentum exhibited in the two panels above the chart and the multi month consolidation suggest distribution.

Let's look "under the hood" of the market:

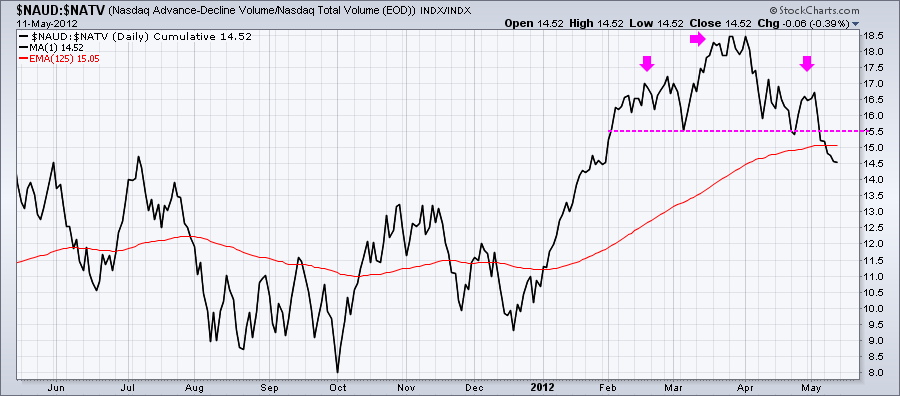

The two charts above are Advance/Decline volume as a percentage of the total volume for both the NASDAQ (above) and the NYSE (below). In essence, they are showing the net advancing volume for both indexes. Without healthy volume it doesn't matter how the price of the index is faring. I've highlighted in pink arrows a clear head and shoulders formation on the NASDAQ chart but that formation is also clearly evident on the NYSE chart. Both charts have violated the neckline of the formation so unless we get a quick turnaround next week we're heading lower.

Both of these charts are showing classic signs of distribution (smart money selling into strength).

Treasuries are confirming what stocks are telling us:

And here's another signal that deflationary forces are gaining the upper hand in the global financial market place:

My regular readers might be getting sick of seeing this chart but the long awaited inverse head and shoulders formation I've been following fell apart this week and Gold fell out of bed! Next stop is $1,500.00. Gold is reacting to the Dollar's price action:

For a longer term perspective of the Dollar, here's a weekly chart:

Finally, here's how commodities are looking this week:

While I seem to be painting a pretty bleak picture for the market over the short to intermediate term I want to emphasize that, my bearish thesis notwithstanding, equities have not yet totally confirmed a downtrend. I'd want to see the Russell and the S&P 500 confirm the Wilshire's price action. Nevertheless, the price action in Treasuries, the Dollar, Gold and commodities are ominous.

What can change this developing negative scenario in a "heartbeat"? Good old central bank liquidity! QE! Money printing!

And let me explain why I believe my bearish thesis may possibly only be short term:

1. Greece - as I've been stating for a number of weeks and what the press has been speculating about this past week, Greece will leave the European Monetary Union. The Greek elections have completely fractured the Greek Parliament and all attempts by the three leading political parties to form a coalition government have failed. This will inevitably lead to another round of elections next month. The problem is that in order for Greece to receive more assistance it needs to decide on another 11 billion Euros in cost cutting. Without a government and the anti austerity mood so prevalent among Greek voters there is, save only by a miracle, no chance of any concerted effort in the Greek government to agree on any cost cutting. Already the EU is withholding some of the money they were going to lend Greece this week as a warning against the Greeks reneging on their commitments.

And a Greek exit from the Union and return to the Greek Drachma, while not in itself threatening a financial implosion,will still put 1/2 trillion Euros of bad debt on the books of the ECB and the IMF, as reported by Sober Look (http://soberlook.com/2012/05/greek-exit-would-convert-over-half.html). Folks, this is about deflationary as you can get!

2. Spain - Spain is turning into another basket case analogous to Greece but perhaps not of the same magnitude. Unemployment is currently at 24% and the economy is in the throes of deep contraction. The Spanish banking system is a shambles and the latest plan to firm up their balance sheets is too little and perhaps too late. The Spanish banking system will probably have to be nationalized which will put all those bad debts on the sovereign's balance sheet. This will inevitable cause more credit downgrades by the rating agencies which will have the net effect of pressuring Spanish bond yields higher. At some point, higher yields get prohibitive to finance which could inhibit Spain from bringing their debt to market. As I've stated in past commentaries, the EU could support a Greek debt bailout and maybe a bailout of Greece and Portugal together but it will not be able to absorb a Spanish bailout.

China - announced late Saturday night another easing of their banking reserve requirements. This was a 50 basis point cut and whether it will stop the economic bleeding in the Chinese economy is open to conjecture. The majority of pundits still hold to a soft landing for the Chinese economy and I'm also of that camp. However, we need to start "landing" soon. And if we get another month of ugly economic reports like April, the odds will start favoring a hard landing for the world's growth engine.

Here's the Shanghai Composite Index as of Friday's close:

As I said above the only factor that can turn around the building deflationary pressures in the global economy is central bank liquidity injections (AKA money printing, QE, etc.) Will central banks act?

I believe that, in one sense, they have no choice. Considering the requirements of a credit based Keynesian world, deflation is not an option. But as I showed in Tuesday's blog post (posted again here for your convenience with a few embellishments) more and more liquidity provided by the FED has been met with diminishing market returns:

Those who hold to the premise that central banks will open the liquidity spigot wide may be disappointed. Certainly there has to be a recognition that all efforts up to this point to bolster the global economy have been met with diminishing returns. Would central bankers actually threaten the global financial system with another avalanche of fiat money which would definitely stoke serious global inflationary pressures? Some say yes; I say no. Let me pose a hypothetical question that will serve to clarify my position on this issue: If you were at a party and you were threatened that the spiked punch bowl would be taken away from you if you over did it would you continue to imbibe at a steady rate? In my opinion, this hypothetical example is analogous to the current situation central bankers are confronted with. Will they be reckless and let their Keynesian presuppositions blind them to the risks of uncontrolled money printing; thereby threatening to destroy the current economic system? Or will they recognize the danger, conform to the notion that we'll be in a muddle through (at best) global economy for about a decade and provide just enough stimulus to buy the time needed for sovereigns and their banking systems to slowly de leverage? I'm betting on the latter and I have some evidences to support my thesis:

- the extreme hesitancy of the ECB to embrace a FED like monetary stimulus (other than the two recent LTROs)

- China unwilling to provide direct fiscal stimulus and monetary stimulus largely confined to reserve ratio cuts.

- the FED's "Operation Twist" was largely a sterilized operation and nothing like the first two QEs.

- the reaction of Gold since last September has been Mr. Market's way of confirming my thesis. Without the inflationary implications of further monetary easing one of Gold's main "legs" are pulled out from under it.

In the short term, if/when Greece exits the EU, there will be a wave of sovereign downgrades from the ratings agencies (Moody's, Fitch and S&P) which will bring substantial pressure to bear on the yields of other periphery debt and this pressure may prevent Portugal and even Spain from participating in public bond auctions. If this occurs it will be responded to by coordinated central bank intervention (ECB & FED) to stem the panic. This will be a temporary boon to the market. But nothing in essence will have changed the macro financial debt picture.

The US economic calendar will be fairly busy this week with:

- Consumer Price Index and Retail Sales on Tuesday

- Housing starts and Industrial Production on Wednesday

- Jobless claims and the Philadelphia FED survey on Thursday

The European economic calendar is also pretty busy this week and I'm not going to highlight every report/event but I'll be especially watching the Italian 10 Year Bond auction on Monday and German GDP on Tuesday.

Have a great week!

NOTHING IN THIS COMMENTARY SHOULD BE CONSTRUED AS AN OFFER OR ADVICE TO BUY OR SELL ANY SECURITIES, OPTIONS, FUTURES OR COMMODITIES. THE OPINIONS ARTICULATED ARE ONLY THIS AUTHOR'S WHO IS NOT A LICENSED INVESTMENT COUNSELOR OR BROKER

No comments:

Post a Comment